Last Friday we played Tambola online. And frankly, I had strong preconceived notions it’s not going to be that usual fun! After all, striking numbers, asking a friend colleague “16 Aaya kya” (Has no 16 been announced?), and cribbing on every time someone claims a reward “mera bas ek rehta tha” (I only needed one number to claim this reward Urrrghh!) are some of my fond memories of the game.

However, the game went superbly well (Yes we have a great HR team :)). But sadly this time I didn’t win any rewards..ahh okay.. that’s a crib for another day! The fun tripled maybe because our expectations at the start were at rock bottom. In simple words, we were craving these fun games. However cliché it may sound but this pandemic has pushed/pulled us to go Digital in every aspect of our daily life!

As digital achieves new high, news ideas have cropped in and a few lost or neglected ones are all ready to take the front seat. One such intriguing idea is the idea of banking without banks and banks without branches. Yes, you heard it right! Banking without Banks and Banks without Branches!

Read: How traditional banks in India are dealing with cryptocurrency?

This as a concept has been around for more than half a decade now but as we start this new decade, individuals (more than any era in the past) are ready and open to digital change that improves their financial lives.

Banking, a sector often accused of being too traditional, conservative, and lazy. (Mental image: lethargic branch staff probably Uncles and Aunties upset with their lives, in their mid 50’s, sipping cups of tea, most of the time on Lunch breaks, and leaving for home at 4pm) has lately seen a fair bit of technology-infused disruption, be it the Zero-contact savings account opening, digital lending, digital payments, or mobile banking the list is endless.

First, let’s define the Neo concept: What are Neobanks?

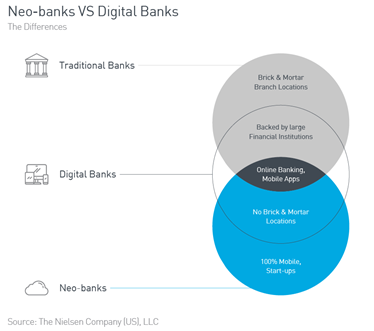

“Neobanks are a new type of direct bank that are fully digital, without physical bricks-and-mortar branches, and are 100% independently owned.”

Source: Nielsen,2019

It is a type of digital bank operating exclusively online, i.e. it does not have physical branch networks. These financial technology firms offer digital services or mobile-only services. It’s a broad umbrella of financial services that beseech today’s tech-savvy customers.

So, Neo Banking in 4 simple words is “Banking beyond physical walls!”

Since I am fond of maths (ahh…show off!). Let’s use the Venn diagrams to understand the position of a Neo-bank in the ecosystem.

How does a Neo bank differ from a traditional bank?

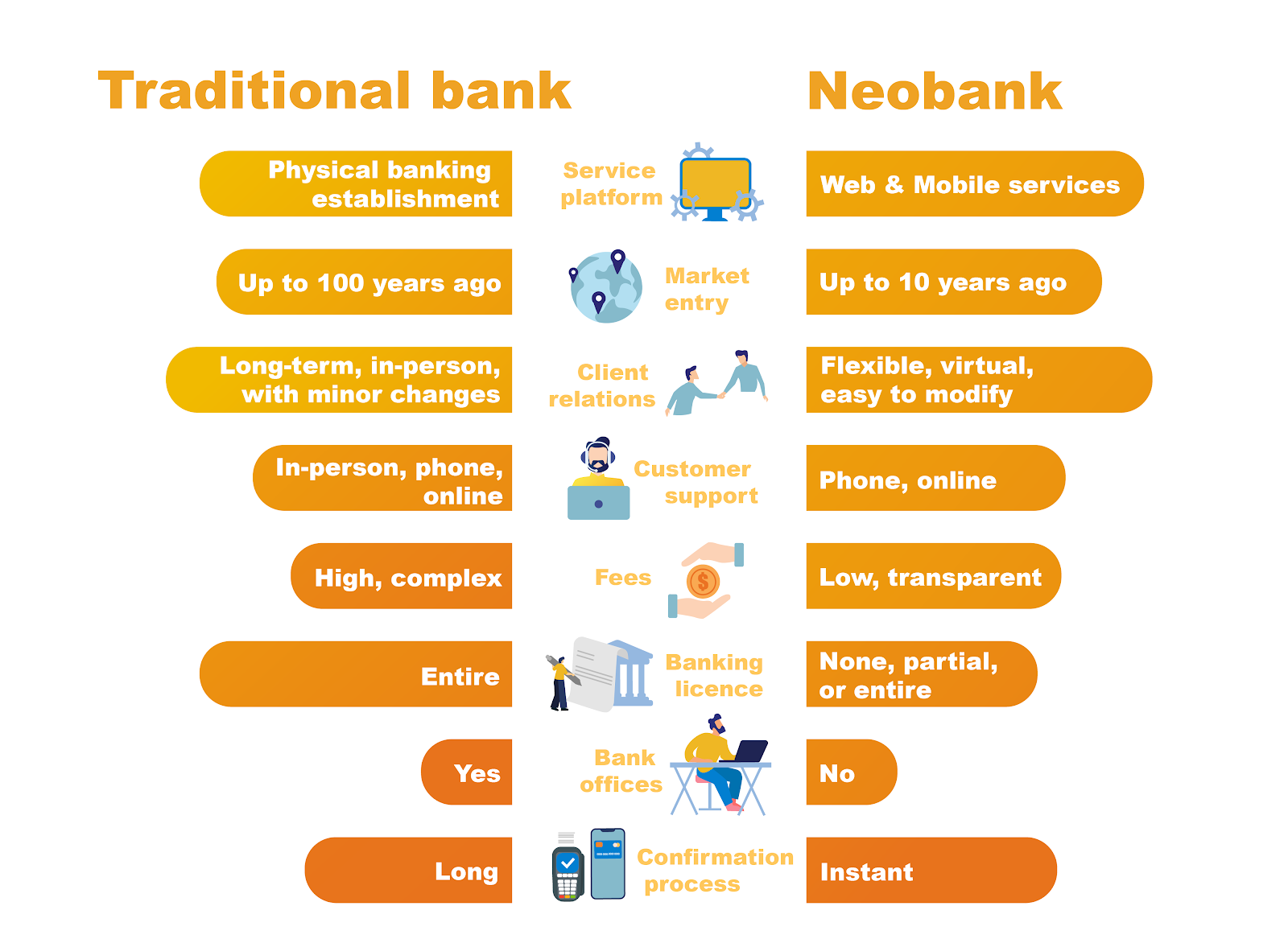

Fundamentally, Neo banks are different from traditional banks in every aspect of their existence from business models to customer care to regulation. Here is quick side by side comparison done by Softensy:

So, Neo Banking in a nutshell is:

1) Banking for tech savvy

Neo banks are proficient in easier customer acquisition- customers include tech savvy millennials, SME and low ticket salaried class, which are not the focus areas of legacy banks.

2) Banking @reduced cost

With a reduction in CAPEX (thanks to no physical branches), customers enjoy competitive pricing with more significant savings.

3) Banking at customer’s convenience

Neo banks are all about customer choices, accessibility, and 24*7 time services.

Read: How Fintech is “Lending” a helping hand?

Neo Banks Globally

Globally the Neo Bank segment is about a decade old. The global Neo-bank market was worth USD 18.6 billion in 2018 and is expected to accelerate at a compounded annual growth rate (CAGR) of around 46.5% between 2019 and 2026, generating around $394.6 billion by 2026. (Source: PwC)

The Neo Banking market is big in the UK, with 15 licenses granted since 2005. 9% of the British adults have a Neo Bank account. Neobanks have nearly tripled their customer base in the past year. From 7.7 million customers in 2018 to almost 20 million in 2019 ― this current growth rate of 150% outpaces the 2% growth for traditional challenger banks and 1% for incumbents.

Neo Banks globally are famous for faster customer acquisition and consumer appeal vs legacy banks. They offer wider products as globally Neo Banks are allowed to take deposits and lend on their own books. However, Profitability and competitive agility remain pressure points for Neo Banks globally.

Roadblocks in the Rise of Neo Banking Startups in India

Currently in India, Neo banks are not allowed to hold customer deposits and neither virtual license is being granted by the RBI since it still maintains its stand on the need for physical presence as per its 2014 guidelines (due to its concerns over cryptocurrency transactions).

So, primarily there are two types of Neo Banks in India.

One, where the Neobank doesn’t have a banking license itself and instead partner up with a traditional bank to provide its products. For instance, NiYO has a partnership with DCB Bank while Open works with ICICI Bank.

While in the second scenario the Neo banks obtain banking licenses themselves to operate fully on their own (of course..not holding customer deposits). As a result, many of these internet-first banks are either partnering with those banks that have licenses or are offering only a few banking services like payments, lending (and not savings) (e.g. Airtel payments banks, Paytm Payments Bank).

Neo-banks are forced to have a symbiotic relationship with traditional banks owing to regulatory policies by the RBI that do not recognize or rather deny the legitimacy of digital-only banking institutions.

Thus, the Neo-banking story in India is partially incomplete!

Future in India

For the longest period of time in human history, it was believed that Earth was the center of the universe until a scientist named Copernicus challenged the priori notion to set in motion the theory that offered an alternate world view and changed the way we understood the universe. Much like how humankind eventually reckoned that the sun as the center of the universe, rightfully, we will have customers at the center of banking (we already are witnessing that shift!).

The growth of Neo banks only promises to be an exciting journey in the next few years with one ultimate winner: the consumer, by way of more choice, better accessibility, and better value. How Neo banks look to leverage their advantages and mitigate their disadvantages, will be one of the most interesting evolutions in banking in the coming years. The outlook is bright and expansive for established Neo banks and new arrivals offering a personalized experience for niche user segments.

Contactless products and services (remember Ranveer’s advertisement!) will take center stage. Neo-Banks in this regard are well-poised to benefit from this trend.

Neo banks are clearly the future of banking as we know it. Thanks to their unwavering customer focus, they have been able to carve a niche for themselves in a relatively short span of time.

Interested in reading our Finance Strategy Stories. Check out our collection.

Also, check out our most loved stories below

IKEA- The new master of Glocalization in India?

IKEA is a global giant. But for India the brand modified its business strategies. The adaptation strategy by a global brand is called Glocalization

Why do some companies succeed consistently while others fail?

What is Adjacency Expansion strategy? How Nike has used it over the decades to outperform its competition and venture into segments other than shoes?

Nike doesn’t sell shoes. It sells an idea!!

Nike has built one of the most powerful brands in the world through its benefit based marketing strategy. What is this strategy and how Nike has used it?

BlackRock, the story of the world’s largest shadow bank…

BlackRock has $7.9 trillion worth of Asset Under Management which is equal to 91 sovereign wealth funds managed. What made it unknown but a massive banker?

Why does Tesla’s Zero Dollar Budget Marketing work?

Touted as the most valuable car company in the world, Tesla firmly sticks to its zero dollar marketing. Then what is Tesla’s marketing strategy?

Microsoft – How to Be Cool by Making Others Cool

Microsoft CEO Satya Nadella said, “You join here, not to be cool, but to make others cool.” We decode the strategy powered by this statement.