“Agar firdaus bar roo-e zameen ast, Hameen ast-o hameen ast-o hameen ast.”

The great Persian poet Amir Khusro wrote these words in appreciation of the sheer beauty of Kashmir. English Translation of this verse is: “If there is a paradise on earth, it is this, it is this, and it is this.”

Analogically, if Amir Khusro was alive and were to describe Ireland, he might have said “if there is a paradise on earth for tax evaders, it is Ireland, it is Ireland and it is Ireland.”

Ireland – Home to Tax Evaders

Ireland, the country, is not only renowned for beers, whiskey, or exotic filming locations in Game of Thrones but also notoriously famous for tax evasion. Ireland has been labeled as a corporate tax haven by various NGOs, academic studies, and research reports.

However, the state rejects all such claims and even the EU commission & OECD have not considered Ireland as a tax haven.

Explore Ireland, Game of Thrones Territory

Though Ireland claims a headline corporate effective tax rate of 12.5% due to the plethora of exemptions, deductions, and allowances, the effective tax rate comes down to the range of 2%-4%. This gap implies that over 60%-80% of corporate tax profits are not being taxed in Ireland.

Ireland employs base erosion and profit shifting (BEPS) tools targeting technology companies and life science sectors that deal in specialized Intellectual property. These IP-based tools enable profit shifting from high tax jurisdiction to low tax jurisdiction, saving billions of dollars in taxes.

Hers a brief explainer on how tax haven works:

Ireland – A Tax Haven for US Technology Companies

Ireland is often touted as a “US corporate tax haven”, especially for these IP-based technology companies. Despite objections by the state, evidence suggests that there is a lot of merit in this argument. The US is a leader in the research and development sector and is home to top tech and life science companies. These US companies, especially technology ones, employ Ireland’s IP-based BEPS tools to shift their non-US revenues to Ireland and evade tax on these incomes, which are discussed below in detail:

Double Irish affair

It is the largest tax avoidance tool in history and was being used by US MNCs since 1980. EU forced Ireland to close the scheme beginning 2015 and gave existing users such as Apple, Google time until 2020 to comply with the new rules. However, the scheme successfully enabled the build-up of non-taxed offshore reserves of over US$1 trillion before closure.

(Pro Advice: Fasten your seat belts as the ride is going to be a bit bumpy for a short while)

Barring certain variations, the basic structure that followed Double-Irish arrangement was as follows:

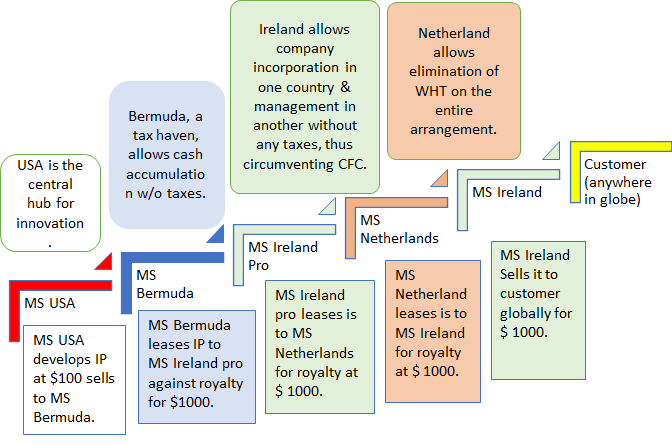

- A US-based technology company (let’s say MS) would develop IP through R&D at the cost of $100.

- MS then sells it to Company MS Bermuda, a Bermuda-based subsidiary of MS, at the cost of $100.

- MS Bermuda revalues it to $1000 and earns a tax-free capital gain of $900. (Bermuda is a tax haven that does not tax capital gains)

- MS Bermuda licenses the IP to Company MS Ireland, an Ireland-based subsidiary of MS Bermuda, for $1000.

- MS Ireland then sells the software (IP) to the customer (anywhere globally) for $1000.

Income and taxes:

- MS Ireland uses the sales revenue to pay a royalty to MS Bermuda. (No income, no tax)

- MS Bermuda receives tax-free royalty income and accumulates cash till perpetuity, and avoids US taxes.

This would have been a fairy tale ending for MS if there were no Controlling Foreign Corporation (CFC) rules in the US. But Uncle Sam has indeed created detailed CFC rules. In this arrangement, when CFC rules kick in, it deems Bermuda to be a sham company and charge US tax on royalty income received by MS Bermuda. So, the entire arrangement fails.

But there is still hope. The world has lawyers and tax experts in their black suits with weapons of paper, pen, and interpretation skills to save the day. Tax experts swirl the magic wand at this juncture and pull out the trick for the greatest tax heist ever. They create another company, MS Ireland Pro, in Ireland such that this company is incorporated in Ireland but managed and controlled from Bermuda.

MS Ireland Pro is placed as a slice between MS Bermuda and MS Ireland in the above ex. MS Ireland Pro, with its unique status of incorporation (in Ireland) and management (in Bermuda), bypasses the CFC rules. US authorities don’t question the structure, and MS earns its entire income tax-free.

Double Irish Dutch Sandwich Principle

However, there’s one problem with the above arrangement that MS Ireland would need to deduct Withholding Tax (WHT) @ 20% on royalty payments to MS Ireland Pro. This puts the entire scheme in jeopardy.

So, lawyers and tax planners do the magic again. This time they introduced a Dutch company, MS Netherlands, in the arrangement between MS Ireland and MS Ireland Pro. Instead of making direct payments, the payment is routed through the Dutch company, MS Netherlands.

There is an arrangement between Ireland and The Netherlands (thru DTAA) under which certain incomes like royalty etc are not taxed. This allows rerouting of royalty income through Dutch companies without WHT obligations of 20%.

This Dutch company, MS Netherlands, is described as a Dutch slice sitting between MS Ireland and MS Ireland Pro, completing the Double Irish Dutch Sandwich Principle.

Capital Allowances for Intangible Assets (“CAIA”) BEPS tool

The Double Irish arrangement came under scrutiny and fire from all sides, and in 2014 finally, the EU forced the Ireland government to get rid of the arrangement. The tax rules were changed and the loopholes of Double Irish arrangement were closed.

Irelands’ successful endeavors with Double Irish and Single Malt tools established it as a conduit offshore financial center for transfer of income to tax-free Caribbean Islands or Malta. However, CAIA enabled Ireland to become the tax-saving terminal in its own being without the use of locations like Bermuda.

The tool allows the intra-group purchase of intangible assets (especially intellectual property rights) and allows to claim capital allowances on IA assets purchased from a group of companies. It doubles the tax shield impact when consideration for IAs purchased is done on a loan plus interest basis and allowing deduction of interest expense on the amount lent.

For example, in Q1 2015, Apple used the CAIA tool when its Irish subsidiary purchased US$300 billion in intangible assets from an Apple subsidiary based in Jersey. Usually, the tax deduction is not allowed for the intragroup purchase of intangible assets globally, but this is not the case with Ireland.

The CAIA tool enabled Apple to write-off the US$300 billion price as a capital allowance against future Irish profits. Simply saying, Apple was able to claim $300 billion as an expenditure, something akin to 80C deductions salaried employee claims in India but without any capping of INR 1.5 lakhs or $300 billion.

However, the CAIA is more powerful, as Apple demonstrated by effectively doubling the tax shield (e.g., to US$600 billion in allowances) via Irish interest relief on the intergroup virtual loans used to purchase the IP.

Although authorities have managed to put a lid on tax strategies like Double Sandwich or Single Malta, the CAIA has made Ireland the biggest paradise for tax evaders with the double effect.

Economic Impact of Ireland BEPS tools

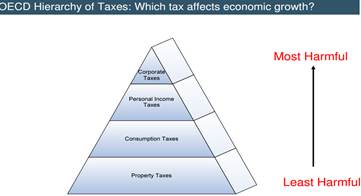

Ireland’s tax policies are based on the OECD hierarchy of taxes which believes corporate taxes are most harmful to economic growth and thus aim to lower them. This has led Ireland to resort to low tax rates and earn it a “coveted” tax haven status. This approach has worked well for the nation and its economy in various ways.

By September 2018, US-controlled corporates were 25 of Ireland’s 50 largest companies, paid 80% of Irish business taxes, directly employed 25% of the Irish labor force, and created 57% of Irish value-add.

These technology companies have been a bane to the economy of Ireland by generating jobs in service sectors of accounting, auditing, tax, legal sector, and establishing Ireland as a global hub of financial services and tech sectors and a major developing nation.

This has also positioned Ireland as a preferred hub for global “knowledge economy” multinationals for selling into EU nations and established Ireland as a gateway for doing business in Europe for US technology companies.

This approach created a few issues for the country as well. In September 2016, Brazil became the first G20 country to “blacklist” Ireland as a tax haven.

This also led to GNP-GDP distortion at an unprecedented scale. CAIA tool artificially inflated GDP per capita and Debt per capita statistics of the country. The economic picture got so distorted by BEPS flows that the Central Bank of Ireland had to use a new indicator modified GNI in 2017.

In 2015, Ireland reported GDP growth of 26.3% which was due to Apple’s implementation of the CAIA tool and not because of any real economic activity. Though apple contributed to the economy by creating jobs, investing money in financial sector and research but the main contribution to GDP growth (over 20% of Irelands GDP) was more of a sham than any real benefit.

EU imposed a fine of EUR 13 Bn on Apple, plus interest, in unpaid Irish taxes on circa €111 billion of profits, for the ten-year period, 2004–2014. It was the largest corporate tax fine in history. However, the Irish state and Apple successfully defended the fine. (Yeah, you read it right Irish state defended the fine imposed on Apple against EU)

Heres’ an explainer video on Apple tax misadventures in Ireland:

Way Forward:

OECD has introduced BEPS action plan for member countries to curb tax evasion practices of MNCs, ensuring that profits are taxed where economic activities generating the profits are performed and where value is created. With support from G20 and OECD members, this move aims to solve the global menace caused by tax heavens.

These tax havens not only promote inequality amongst nation-states but also among citizens. An arrangement would be really unfair and unethical if it let go of the most profitable companies earning billions of dollars without charging any taxes and small businesses paying over 30-40% taxes on their small incomes.

The OECD BEPS action plans and the recent decision of G7 countries to establish a global minimum tax rate of 15% are steps in a positive direction.

While you continue to wonder why you are paying taxes 30% taxes plus all sorts of cesses, the most profitable technology companies are not just having a free lunch but are celebrating once in a millennium kind of a grand party in Ireland.

-AMAZONPOLLY-ONLYWORDS-START-

Also, check out our most loved stories below

Why did Michelin, a tire company, decide to rate restaurants?

Is ‘Michelin Star’ by the same Michelin that sells tires, yes, it is! But Why? How a tire company evaluations became most coveted in the culinary industry?

Johnnie Walker – The legend that keeps walking!

Johnnie Walker is a 200 years old brand but it is still going strong with its marketing strategies and bold attitude to challenge the conventional norms.

Starbucks prices products on value not cost. Why?

In value-based pricing, products are price based on the perceived value instead of cost. Starbucks has mastered the art of value-based pricing. How?

Nike doesn’t sell shoes. It sells an idea!!

Nike has built one of the most powerful brands in the world through its benefit based marketing strategy. What is this strategy and how Nike has used it?

Domino’s is not a pizza delivery company. What is it then?

How one step towards digital transformation completely changed the brand perception of Domino’s from a pizza delivery company to a technology company?

BlackRock, the story of the world’s largest shadow bank

BlackRock has $7.9 trillion worth of Asset Under Management which is equal to 91 sovereign wealth funds managed. What made it unknown but a massive banker?

Why does Tesla’s Zero Dollar Budget Marketing Strategy work?

Touted as the most valuable car company in the world, Tesla firmly sticks to its zero dollar marketing. Then what is Tesla’s marketing strategy?

The Nokia Saga – Rise, Fall and Return

Nokia is a perfect case study of a business that once invincible but failed to maintain leadership as it did not innovate as fast as its competitors did!

Yahoo! The story of strategic mistakes

Yahoo’s story or case study is full of strategic mistakes. From wrong to missed acquisitions, wrong CEOs, the list is endless. No matter how great the product was!!

Apple – A Unique Take on Social Media Strategy

Apple’s social media strategy is extremely unusual. In this piece, we connect Apple’s unique and successful take on social media to its core values.

-AMAZONPOLLY-ONLYWORDS-END-