Let’s start with a quick recap of our previous article. Where we had a chat over coffee about Value (Intrinsic Value) and Valuation (Market Value). And approach to asset valuation under the Discounted Cash Flow (DCF) approach using ‘The CCD Wakcup Orion’. We highly recommend reading that article.

For a keen mind, it would also have been enticing to notice the similarity of approach between ‘DCF approach to Valuation’ and ‘Net Present Value technique (NPV) in investment decisions making’, a technique that we are already well-versed with.

We generally agree that a Discounted Cash Flow (DCF) approach is an intuitive way of getting a sense of the REAL VALUE (expected) of any asset. After all, the Discounted Cash Flow approach fundamentally relies on the USAGE of the asset AND the extent of FUTURE ECONOMIC BENEFITS generated out of it.

From the above simplification, the Valuation of Business Entities using the Discounted Cash Flow Approach looks pretty straightforward. And simple if not an absolute cakewalk, right? Now that you are suckered into it, a few fundamental (googly) questions to get you thinking and probably stump you.

- Can business entity be equated to an ‘asset’?

- If you convince yourself that it is an asset, then how do we determine Future Economic Benefits?

- What exactly do we mean by ‘FUTURE’ (how many years going forward)?

- What would be an appropriate discount rate to determine the Present Value of Future Economic Benefits?

Read: BlackRock, the story of the world’s largest shadow bank

In this article, Lets’ explore the complexities involved in applying the Discounted Cash Flow approach to determine the Intrinsic Value of a Corporate Entity by exploring the googly questions. And get a proper picture of the Discounted Cash Flow approach before going forward.

In our next article, ‘Valuation of Coffee Day – In a Hypothetical Scenario’ we can continue our love for coffee and try applying the DCF approach in valuing the company that owns the iconic ‘Café Coffee Day’ chain, Coffee Day Global Limited (CDEL).

The First Googly: Can a business entity be equated to an ‘asset’?

Yes, absolutely…why not?

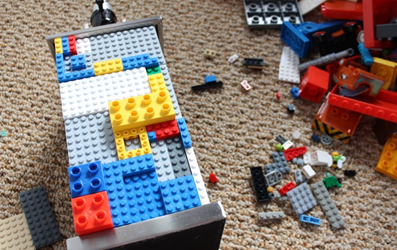

The only adjustment to the thought process is to think of a Business Entity as this giant LEGO STRUCTURE. Just as the Lego Blocks can be combined together to form any Lego Model, a Business Entity can be viewed as multiple assets (Land, Building, Plant & Equipment etc.) combined together to execute the operations and generate Economic Benefit (to be discussed as Free Cash Flows going forward) from them.

While we are getting a hang of asset clusters, we should look at the segregation of assets into Operating Assets and Non-Operating Assets for the purpose of the Discounted Cash Flow Approach. This is primarily to highlight the difference in treatment in their valuation.

In the above picture, it can be noticed that some of the Lego Bricks are used in building the Lego Model. While some are left out and are not used. The value of the used lego bricks reflects in the Lego Model made. That does not mean that those unused Lego Bricks are free or does not have any value. You would still have to pay for all of them when you are buying it. 🙂

Read: LEGO – Powered by the Customers’ Inventiveness

| Take away 1: For Operating Assets = Value is Economic Benefits (PV of Free Cash Flows) generated from them For Non-Operating Assets =Market Value/Realizable Value of all such non-operating Assets |

Using the LEGO analogy to explain the Assets; some of the assets (also called the VALUE ASSETS or the Operating ASSETS) are used in operations and their Value is reflected in the future free cash flows generated and some of them may not be used directly in the operations of business entity (Eg: Land purchased for Investment purpose; Excess Cash parked in FDs etc.). These Assets are called Non-Operating Assets. Their Value is reflected in the market value or their realizable value.

| On a side note, it is worthwhile to check on the proportion of ‘operating assets to total assets’ as this will give sense of value assets in the business and quality of investment decision making of the management. Also, it is worthwhile to mention that DCF Approach would be best suited with the proportion of ‘operating assets to total assets’ is higher as significant value is derived from the Future Economic Benefits derived from them. |

The Second Googly : How do we determine Future Economic Benefits of a business Entity?

This is literally a million dollar question.

For the purpose of DCF Valuation, We will consider the narrow interpretation of ‘Economic Benefits’ as equivalent to the ‘Free Cash Flows’ generated by using the operating assets in the business operations.

| Economic Benefits = Free Cash Flows generated in the business. |

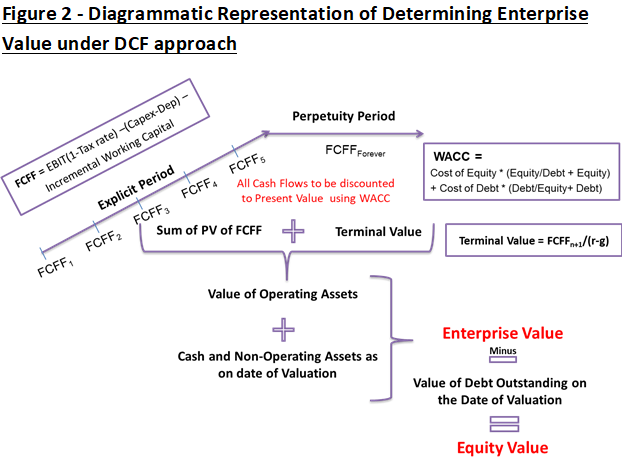

Free Cash Flows can be further classified into Free Cash Flows to the Firm (FCFF) and Free Cash Flows to Equity (FCFE) depending upon the Type of Value being arrived at.

Wait, what? Can we determine more than one type of Value under Discounted Cash Flow method?

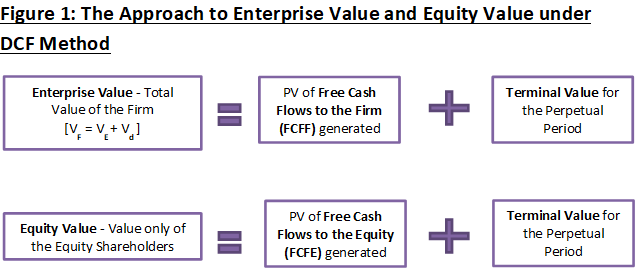

A short answer to the question is YES. Two types of values can be determined under DCF Approach i.e. ENTERPRISE (Firm) VALUE and EQUITY VALUE. Refer to Figure 1 at the end of the article for an overview of the concept. The long version of it is for discussion at another time.

The more important question is the concept of ‘Free Cash Flows’. What is Free Cash Flow?

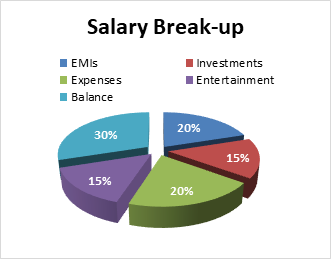

Let us take a simple example of SALARY credited to account. Yeah, the magic phrase that can light up the eyes and mood of anyone. Say, we have a salary of INR 10 Lakh per Month (no loss in dreaming big) and out of which the fixed and planned allocations are as given in the Chart.

Out of the total salary received, around 70% is blocked (encumbered) towards various commitments and only 30% is available for free use as may be desired.

From the example, if the total salary of INR 10 Lakhs is the Gross Cash Flow and the Balance 3 Lakhs i.e. 30% of 10 Lakhs is the Free Cash flow.

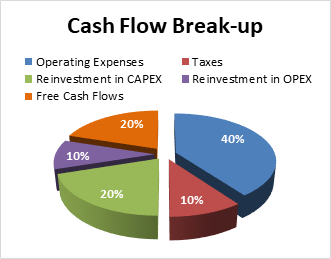

From a business perspective, Free Cash Flows for each year represent the ‘adjusted operational profit’ (NOPLAT) subject to further deductions of obligations for future capital expenditure and future incremental working capital requirements.

The computation of FCFF and FCFE should a part of our follow-up article on ‘Valuation of Coffee Day – A Hypothetical Scenario’

| Take away 2: Cash Flows are NOT EQUAL to the Revenues of the business entity Cash Flows are NOT EQUAL to the Net Profit of Business Net Cash Flows for the business entity is the ‘Operating Profit Adjusted for Non-cash items like Deprecation (and) Reinvestment in CAPEX and Incremental Working Capital’ for future operations |

The Third Googly : What exactly do we mean by ‘FUTURE’ in ‘Future Economic Benefits’?

In our ‘CCD Wakcup Orion’ example, we assumed the life of the asset is 3 years or 5 years at a maximum. This is consistent with the general assumption that ‘Individual Assets have a finite life and the forecast period for cash flows covers the finite lifetime of the asset.

However, the fundamental assumption on the life of a business entity is that it is ‘going concern’ i.e. the business continues operations into the foreseeable future. In simple terms, ‘Business entity has a perpetual life’. This assumption creates a situation where it is difficult to predict the number of years into the future for which Free Cash Flows are to be computed and hence, the concept of Perpetuity is introduced.

Read: The Nokia Saga – Rise, Fall and Return

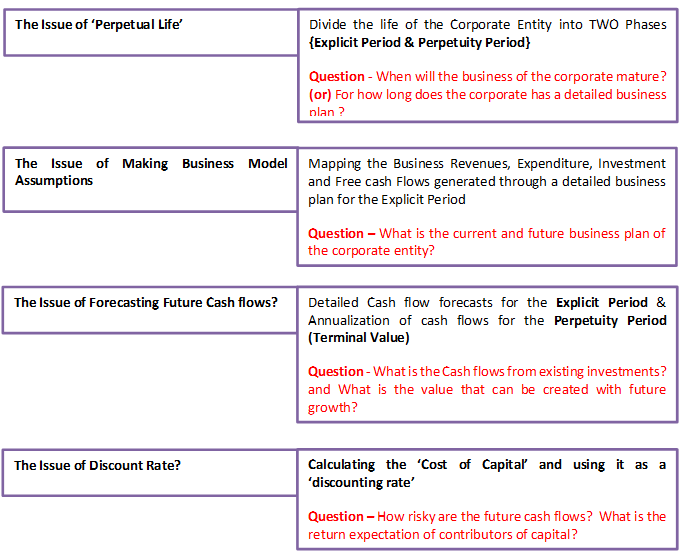

Under this concept, the life of the business entity (Period for forecasted cash flows) is split into Explicit Period and Perpetuity Period.

Explicit Period – It can be understood as the period of a high growth phase for a company before its operations become stable. i.e. Maturity Phase (or) If the company is already a fairly large and mature company, then the period for which the company has a detailed business plan.

During the Explicit Period, A detailed ‘business plan exercise’ is made. To map the Business Revenues, Expenditures, Investments into CAPE & OPEX, and extent of Free cash Flows generated in the forecast period.

Perpetuity Period – The Period beyond the explicit period is called Perpetuity. It is the phase where the company experiences relatively stable cash flows (or) Operating Cycles.

| Take away 3: Explicit period – Period of growth (or) period for which there is detailed business plan There is no fixed number of years that can be counted as Explicit Period. t is dependent upon case to case. However, a general rule of thumb is atleast 3 to 5 years period. Perpetuity period – the future period beyond Explicit Period FCFF during Explicit period – To be determined by preparing detailed business plan Terminal Value – the aggregate of ‘annualized cash flows’calculated using Gordon’s growth model |

For the Perpetuity Period, the cash flows for the (n+1)th Year, I.e. the year after last year of explicit period are annualized. The Annualized free cash flows computed is called the TERMINAL VALUE using Gordon’s growth model. (The approach to computation to be addressed in the next article)

The Fourth Googly: What would be an appropriate discount rate to determine the Present Value of Future Economic Benefits?

With regard to the discount rate to determine the Present Value (PV) of Free Cash Flows, there are two pertinent questions. Why should we discount Free Cash Flows to Present Value? And, what should be an appropriate discount rate?

For the WHY, The first reason is to give effect to the ‘Time Value of Money’. And the second reason is to bring all cash flows originating in different years in the future onto a single point in time. (i.e Date of Valuation). This brings Parity and Comparability to Free Cash Flows Measurement.

For the WHAT, the answer is relatively simple. For beginners, lets’ just say that the appropriate discount rate is the effective cost of capital (or) Weighted Average Cost of Capital (WACC). WACC as a hurdle rate represents the minimum opportunity cost of funds to the business entity.

The real and the challenging question however is, HOW should it be calculated? What are the various components of WACC? And what are the various aspects to be considered while arriving at the cost of funds happens to be an interesting area of study.

| Take Away 4 Discounting Rate = Generally WACC is considered as an appropriate Discount Rate Discounting Rate depends on the Riskiness of the cash flows. Higher the Risk, higher is the discount rate |

The Conclusion

To summarize the outcome of the discussion from the 4 questions above –

Interested in reading more about Top Finance Strategies? Check out our collection.

Also check out our most loved stories below

IKEA- The new master of Glocalization in India?

IKEA is a global giant. But for India the brand modified its business strategies. The adaptation strategy by a global brand is called Glocalization

Why do some companies succeed consistently while others fail?

What is Adjacency Expansion strategy? How Nike has used it over the decades to outperform its competition and venture into segments other than shoes?

Nike doesn’t sell shoes. It sells an idea!!

Nike has built one of the most powerful brands in the world through its benefit based marketing strategy. What is this strategy and how Nike has used it?

Domino’s is not a pizza delivery company. What is it then?

How one step towards digital transformation completely changed the brand perception of Domino’s from a pizza delivery company to a technology company?

Why does Tesla’s Zero Dollar Budget Marketing work?

Touted as the most valuable car company in the world, Tesla firmly sticks to its zero dollar marketing. Then what is Tesla’s marketing strategy?

Microsoft – How to Be Cool by Making Others Cool

Microsoft CEO Satya Nadella said, “You join here, not to be cool, but to make others cool.” We decode the strategy powered by this statement.

Statement")