Imagine you enter a gadget store with plenty of advanced gadgets. You are a gadget freak! You are excited! But suddenly, you see the price tag. And then you see your bank account. You get disappointed because it’s the end of the month. Who would have thought just a decade earlier that you could buy stuff without having a single penny in your account?

Buy Now Pay Later companies such as Klarna in Europe, Afterpay in Australia, or Affirm in the US make this possible through innovative business models. Affirm is on a mission to deliver honest financial products that improve lives. That made me so curious about Affirm and what made it so successful in reaching a valuation of $11 bn in just a decade. I was interested to learn about Affirm’s business model and how Affirm makes money?

Let’s first clear some basics.

What is Affirm?

As per Investopedia, Buy Now, Pay Later (BNPL) is a type of short-term financing that allows consumers to make purchases and pay for them at a future date, often interest-free. Also referred to as “point of sale installment loans,” BNPL arrangements are becoming an increasingly popular payment option, especially when shopping online.

Headquartered in California, Affirm was founded in 2012 by Max Levchin, Nathan Gettings, Jeffrey Kaditz, and Alex Rampell to make it easier for its users to make intelligent choices with their wallets.

In October 2017, the company launched a consumer app that allowed loans for purchases at any retailer. The company announced a partnership with Walmart in February 2019. Under the partnership, Affirm is available to customers in-store and on the Walmart website. Affirm has partnered with e-commerce platforms including Shopify, BigCommerce, and Zen-Cart. Affirm is also Amazon’s exclusive buy now, pay later partner in the United States through January 2023

Affirm believes that legacy payment systems and traditional risk and credit underwriting models can be harmful, deceptive, and restrictive to consumers and merchants. Affirm also considers that these conventional systems are not well-suited for increasingly digital and mobile-first commerce and are built on legacy infrastructure that does not support the innovation required for modern commerce to evolve and flourish.

Affirm claims that its platform addresses these problems with a point-of-sale payment solution for consumers, merchant commerce solutions, and a consumer-focused app.

Buy Now Pay Later is not a new concept. Short-term and Long-term credit lending is old as 1950. Your typical credit card also follows this business model. Affirm is a new version of this “Buy Now Pay Later” business model. New-age fintech like Affirm found a more efficient, consumer-friendly, and cheaper way. Affirm is committed to helping consumers shop, pay, and bank with ease.

Let’s now try to understand the various aspects of Affirm’s business model.

[icon name=”lightbulb”] Australian Afterpay is championing the “buy now pay later” facility while charging merchants for the service and security. So what is Afterpay’s business model?

What makes Affirm’s business model so unique?

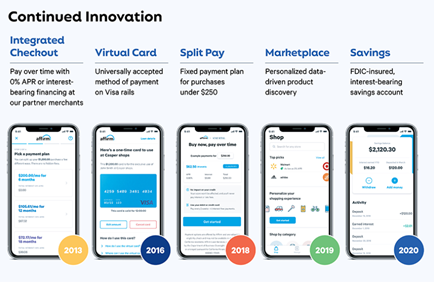

Affirm enables consumers to confidently pay for a purchase over time through its next-generation commerce platform and partnerships with originating banks, with terms ranging from one to sixty months.

When a consumer applies for a loan through Affirm’s platform, the loan is underwritten using its proprietary risk model, and once approved, the consumer selects their preferred repayment option. Most loans are funded and issued by Affirm’s originating bank partners.

Repeat consumers took out approximately 64% of loans facilitated through Affirm during 2020. Affirm has a Net Promoter Score of 78, far exceeding the industry average of 44.

Let’s understand the Value Proposition of Affirm

Consumers: Affirm empowers customers to pay for a product in fixed installments with no additional costs instead of paying up front. This increases consumers’ purchasing power and gives them more control and flexibility. Customers can make four interest-free payments every two weeks. Additionally, a transaction with Affirm does not affect credit score.

Unlike traditional banks that charge compound interest, Affirm charges simple interest. This means consumers pay fixed amounts of interest that they agree to upfront, and the interest never compounds. As of 2021, Affirm had 7.1Mn customers who transacted $8.3 bn in 2021.

Even if a merchant is not registered with Affirm, consumers can still use Affirm. Affirm facilitates the issuance of virtual cards directly to consumers through its app, allowing them to shop with merchants that may not yet be fully integrated with Affirm.

Merchants: Affirm offers merchants a commerce solution that enhances demand generation and customer acquisition. Affirm empowers merchants to promote and sell their products, optimize their customer acquisition strategies, and drive incremental sales.

Affirm’s payment solutions allow merchants to solve affordability for their customers, providing a revenue accelerator while avoiding discounting and other expensive marketing and promotional channels.

Affirm provides merchants valuable product-level data and insights to better inform their marketing strategies and add value throughout the complete customer lifecycle, from acquisition to conversion to repeat transactions. As of 2021, Affirm has 29,000 merchants.

What competitive advantages are strengthening the business model of Affirm?

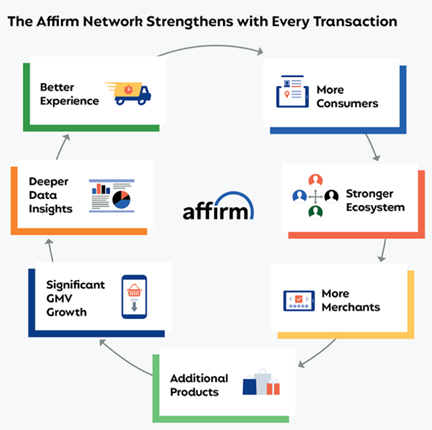

Strong Network Effects: Affirm’s flywheel starts with more awareness among consumers. The more significant is the consumer ecosystem, the more valuable it is to merchants, and the more compelling it is for merchants to offer Affirm as an option. More merchants bring more choices for customers, attracting new customers. Hence the flywheel continues.

Technology Infrastructure & Compounding power of data: Affirm uses machine learning, artificial intelligence, cloud-based technologies, and other modern tools to create differentiated and scalable products. Leveraging these technologies, Affirm is using data to inform its analysis and decision-making, including risk assessment, in a way that empowers consumers and generates value for merchants and funding sources.

Proprietary Risk Model: Affirm claims that its risk model assesses risk better than its competitors. Its integration with merchant partners allows Affirm to consider the consumer’s product when it assesses a credit application. As a result, the delinquency rate for Affirm (refers to the percentage of loans that are past due) is just 1.1%, whereas the average rate for banks is 1.78% in the US.

[icon name=”lightbulb”] How is the European Klarna championing “Buy Now Pay Later”?

How Does Affirm make money?

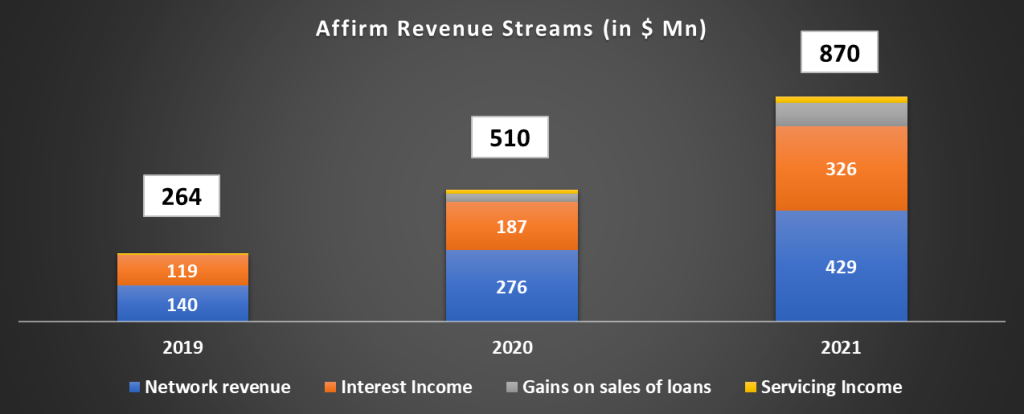

Affirm’s presence at checkout ensures that it remains top-of-mind, allowing it to acquire consumers directly via merchants and sustain a highly efficient go-to-market strategy. Affirm has also leveraged partnerships to drive growth and merchant expansion. Now let’s analyze a million-dollar question: how does Affirm make money? Affirm makes money through four revenue streams: network revenue, interest income, gains on sales of loans, and servicing income. Now, let’s break each revenue stream.

1. Network Revenue: Network Revenue makes ~45-50% of revenue for Affirm. Network revenue comprises two streams: merchant network revenue and virtual card network revenue.

- Merchant partners are charged a fee on transactions processed through the Affirm platform. Merchant fees depend on the individual arrangement between Affirm and each merchant. Merchant revenue makes 40-45% of total revenue for Affirm.

- A smaller portion (4-6%) of Affirm’s revenue comes from its Virtual Card product. Consumers can apply for a virtual debit card through the Affirm app and, upon approval, receive a single-use virtual debit card to be used for their purchase online or offline at a non-integrated merchant. The non-integrated merchants are charged interchange fees by the issuer processor for virtual debit card transactions, as with all debit card purchases, and the issuer processor shares a portion of this revenue with Affirm.

2. Interest Income: Affirm also makes money (~35-40% of revenue) through interest earned on loans facilitated on its platform. Interest income includes interest charged to consumers over the consumers’ loans based on the principal outstanding.

3. Gains on sales of loans: Affirm sells a portion of the loans it originates or purchases from the originating bank partners to third-party investors. Affirm makes money on such loans through the difference between the proceeds received at the date of sale and the loan’s carrying value.

4. Servicing income: Affirm also makes money by providing professional services to manage loan portfolios on behalf of its third-party loan owners. This stream contributes 2-3% to the total revenue of Affirm.

Because consumers are never charged deferred or compounding interest, late fees, or penalties on the loans, Affirm does not make money from its consumers’ mistakes or misfortunes.

What’s the latest at Affirm?

Affirm went public in 2021 by offering a share price of $49 to raise $1.2 bn. On the opening day itself, it soared to $100, but as of writing this story, Affirm’s stock is down by 66%, not keeping investors very happy.

Affirm has a substantial opportunity to increase its share of the e-commerce market, grow its offline business at merchants, and continue to displace merchants’ customer acquisition and marketing spend. Affirm has formed partnerships with huge merchants, including Peloton Interactive, Walmart, Amazon, and Shopify.

In 2020, Affirm partnered with Shopify on Shop Pay Installments to expand its platform’s number of merchants and consumers significantly. Affirm in a press release mentioned that One in four merchants that used Shop Pay Installments during its early access saw 50% higher average order volume than other payment methods.

In Jan ’22, Affirm launched a super app to become a one-stop destination for all shopping needs and effectively manage their finances. Clearly shows the ambitious plans of the company.

Affirm wants to define the future of commerce and payments through its innovative model. But with the solid emergence of Buy now pay later companies and Affirm not showing profitability yet, it would be interesting to see what lies in the future for Affirm’s business model.