With $3.6 trillion of consumer credit originating between April 2019 and March 2020, credit is a cornerstone of the U.S. economy. Access to affordable credit is central to unlocking upward mobility and opportunity. Reducing the price of borrowing for consumers can dramatically improve millions of people’s quality of life.

The first generation of online lenders focused on bringing credit online. Standing in line at a bank branch and waiting weeks or months for a decision was no longer necessary. While they got the credit process online, they inherited the decision frameworks that banks had used for decades and did not address the more rewarding and challenging opportunity of reinventing the credit decision.

Many borrowers suffer from the effects of inaccurate credit models. The FICO score was invented in 1989 and remains the standard for determining who is approved for credit and at what interest rate. While FICO is rarely the only input in a lending decision, most banks use simple rules-based systems that consider only a limited number of variables.

Unfortunately, because legacy credit systems fail to identify and quantify risk correctly, millions of creditworthy individuals are left out of the system, and millions pay too much to borrow money.

Upstart came up with a solution. Upstart leveraged the power of AI to develop an income and default prediction model to determine the creditworthiness of a potential borrower. As strategy enthusiasts, we decided to evaluate various aspects of Upstart’s business model. We will also look at how does Upstart work and make money? We will also do a competitor analysis for Upstart.

What is Upstart? How does Upstart work?

Upstart, founded in 2012, is an AI lending platform that partners with banks and credit unions to provide consumer loans using non-traditional variables, such as education and employment, to predict creditworthiness.

The founding team includes Dave Girouard, former President of Enterprise Google, Paul Gu, a Thiel Fellow, and Anna Counselman, former Manager of Global Enterprise Customer Programs and Gmail Consumer Operations at Google.

Before going public via IPO, Upstart raised $125 Million in 4 rounds from various investors. Let’s now understand how Upstart works.

Upstart is a cloud-based AI lending platform. AI lending enables a superior loan product with improved economics that can be shared between consumers and lenders. Upstart aggregates consumer demand for high-quality loans and connects it to the network of Upstart AI-enabled bank partners.

Consumers on Upstart benefit from higher approval rates, lower interest rates, and a highly automated, efficient, all-digital experience. Bank partners benefit from access to new customers, lower fraud and loss rates, and increased automation throughout the lending process.

Upstart leverages AI’s power to quantify a loan’s actual risk more accurately. Upstart’s discrete AI models target fee optimization, income fraud, acquisition targeting, loan stacking, prepayment prediction, identity fraud, and time-delimited default prediction.

These AI models incorporate more than 1,600 variables and benefit from a rapidly growing training dataset with more than 21.6 million repayment events.

Upstart’s AI models are provided to bank partners within a consumer-facing cloud application that streamlines the end-to-end process of originating and servicing a loan and integrates it into a bank’s existing technology systems.

To summarize, the business model of Upstart works on a platform that connects consumers, banks, and institutional investors through a shared AI lending platform.

How does Upstart make money? What is the business model of Upstart?

Value Proposition

Consumers:

- Higher approval rates and lower interest rates- A study showed that Upstart’s AI model approves 27% more borrowers than high-quality traditional lending models, with a 16% lower average APR for approved loans.

- Superior digital experience- Whether consumers apply for a loan through Upstart.com or directly through a bank partner’s website, the application experience is streamlined into a single application process. In 2021, 69% of Upstart-powered loans were instantly approved with no document upload or phone call required.

Bank Partners:

Upstart targets a wide range of small, medium, and large banks and credit unions with an appetite to invest in improved underwriting, digital originations, and unsecured lending. As of 2021, Upstart had 38 bank partners.

- Competitive digital lending experience- Upstart provides regional banks and credit unions with a cost-effective way to compete with the technology budgets of their much larger competitors.

- Expanded customer base- Upstart refers customers that apply for loans through Upstart.com to its bank partners.

- Lower loss rates by almost 75% while keeping approval rates constant.

- New product offerings- Upstart helps banks provide a product their customers want rather than letting customers seek loans from competitors.

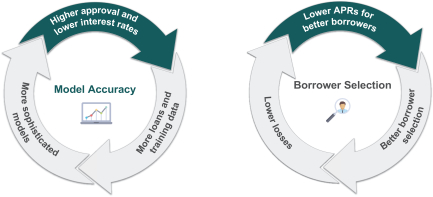

Upstart’s AI Flywheel

Upstart connects consumers, banks, and institutional investors through a shared AI lending platform. Because AI is a new and disruptive technology, and banking is a traditionally conservative industry, Upstart aim is to allow banks to take a prudent and responsible approach to assess and adopt the platform.

On the consumer side, Upstart aggregates demand on its platform, where consumers are presented with bank-branded offers from bank partners. This way, Upstart benefits banks adopting its AI lending technology. Bank partners can also offer Upstart-powered loans through a bank-branded interface on their website or mobile application.

On the funding side, Upstart’s bank partners can retain loans that align with their business and risk objectives.

How does NerdWallet make money: Business Model & Competitor analysis

Marketing

Upstart’s growth and marketing initiatives and strategies are primarily focused on bringing potential borrowers to Upstart.com, where they can learn if they qualify for a loan from one of Upstart’s bank partners and on what terms in only a few minutes.

Upstart’s consumer acquisition channels combine a mix of online and offline and paid and unpaid channels. Upstart’s largest channels include:

- Marketing affiliates—A variety of online media partners, such as loan aggregators, send Upstart traffic on a cost-per-origination basis.

- Direct mail— Upstart targets individuals who both qualify for and may need an Upstart-powered loan. Analyzing an individual’s credit data to target and mail prescreened offers of credit gives this channel a meaningful data advantage over other channels.

- Organic traffic— As Upstart’s brand recognition and reputation grow, more potential borrowers come directly to Upstart.com simply by word of mouth.

- Email marketing— Upstart has an automated email program that sends customized messages and reminders to potential borrowers to encourage them to complete their loan application once they have created accounts.

- Online advertising—Search engines and social channels enable targeted outreach to potential borrowers with specific messages.

- Podcast advertising- Upstart purchases advertising placements on podcasts with a listener base that overlaps with Upstart’s target consumer base.

How does Upstart make money: revenue model

Upstart made $848 Million in 2021. Upstart primarily makes money by charging referral fees from banks for each loan referred through Upstart.com and originated by a bank partner, platform fees for each loan originated, and loan servicing fees as consumers repay their loans.

As a usage-based platform, Upstart targets positive unit economics on each transaction, resulting in a cash-efficient business model with high growth rates and profitability. Following is the structure of revenue streams through which Upstart makes money.

| Revenue Streams (in Thousand $) | 2019 | 2020 | 2021 |

| Referral Fees (1.1) | 90,672 | 1,33,425 | 4,97,996 |

| Platform Fees (1.1) | 53,383 | 66,832 | 2,28,165 |

| Servicing & Other Fees (1.2) | 15,792 | 28,343 | 75,114 |

| Revenue from Fees (1) | 1,59,847 | 2,28,600 | 8,01,275 |

| Interest income and fair value adjustments (2) | 4,342 | 4,816 | 47,314 |

| Total Revenue | 1,64,189 | 2,33,416 | 8,48,589 |

Revenue from Fees, Net (1)

This a significant (95%) revenue-generating segment in which Upstart makes money from two sub-segments: Platform and Referral Fees, Net and Servicing, and Other Fees, Net.

1.1. Platform and Referral Fees, Net: Upstart charges bank partners platform fees in exchange for usage of its AI lending platform, which includes the collection of loan application data, underwriting of credit risk, verification and fraud detection, and the delivery of electronic loan offers and associated documentation. Upstart also charges referral fees to its bank partners in exchange for the referral of borrowers from Upstart.com.

1.2 Servicing and Other Fees: Net Servicing fees are calculated as a percentage of outstanding principal and are charged monthly to any entities holding loans facilitated through Upstart’s platform to compensate Upstart for activities it performs throughout the loan term.

Upstart currently acts as a loan servicer for substantially all outstanding loans facilitated through the Upstart platform. Upstart charges bank partners and institutional investors for collection agency fees related to their outstanding loan portfolio. Upstart also charges fees for establishing and facilitating Upstart co-sponsored securitization transactions and receives certain ancillary fees.

Interest Income and Fair Value Adjustments (2)

Net Interest income and fair value adjustments are comprised of interest income, interest expense, and net changes in the fair value of financial instruments.

Major Competitors for Upstart

Consumer lending is a vast and competitive market. Upstart competes with other sources of unsecured consumer credit, including banks, non-bank lenders (retail-based lenders), and other financial technology lending platforms.

Because personal loans often serve as a replacement for credit cards, Upstart also competes with the convenience and ubiquity that credit cards represent. On the bank partnership side, Upstart competes with various technology companies that aim to help banks with the digital transformation of their business, particularly with all-digital lending.

This includes new products from legacy bank technology providers and more recent companies focused entirely on lending software infrastructure for banks.

Upstart also faces competition from banks or companies that have not previously competed in the consumer lending market, including companies with large and experienced machine learning teams and access to vast amounts of consumer-related information that could be used in developing their credit risk models.

The network effects generated by Upstart’s AI models provide a significant competitive advantage—more training data leads to higher approval rates and lower interest rates at the same loss rate. The most significant competitors for Upstart are TurnKey Lender, Finflux, Sageworks Lending, and Sofi.